Several years ago while tuning into Dateline on NBC, I watched as they conducted one of their typical undercover operations.

Several years ago while tuning into Dateline on NBC, I watched as they conducted one of their typical undercover operations.

This one was a bit different though and more closer to home as they were running sting operations on financial advisors.

To be clearer, it was more on independent life insurance agents that were pitching equity indexed annuities to seniors.

At the time I had only been in the business for around four years, and while I was familiar with fixed annuities and variable annuities, I didn’t quite understand what equity indexed annuities were all about.

The gist of the Dateline Special was showing how crooked financial advisors (aka advisors I would like to punch in the face) were using every sales tactic possible to try to generate a sale, otherwise known as a big fat commission.

While I have no problem with anybody trying to earn a living, I do have a problem with someone trying to line their pockets while putting some else’s best interest out of sight. And that’s what these advisors were doing, selling equity indexed annuities while not conveying the whole truth.

At that point in time I got a really bad taste from equity indexed annuities. I have to confess, I still didn’t know much about them, though with Dateline promoting them as the worst investment product ever made, I decided it would be in my best interest to stay away.

Note: I want to stress here that these advisors weren’t selling an inferior product. In the right situation, Equity Index Annuities can make sense. In the Dateline sting situations, these advisors were not being truthful with how these products really worked.

In the market collapse of 2008, equity indexed annuities have become much more popular.

I’ve talked to several individuals that have purchased them merely for the fact that they are fed with the stock market.

They are looking for a guarantee and don’t mind locking up their money for an extended period of time while also taking a lower interest rate in exchange for less risk and volatility.

Knowing that I should be versed on how these products worked, I knew that I should start doing some research.

Sharing the Basics

With this post I wanted to share some of the basics of how an equity indexed annuity works and to see if it might be a good investment for you.

I also have a loyal Good Financial Cents reader who is a big fan of equity indexed annuities, and I’ve asked him to share his reasoning on why he purchased them for his own retirement planning (he’ll be sharing in the comments).

What is a Fixed or Equity Indexed Annuity?

Good question.

Like all other annuities, an equity indexed annuity is a contract between you and the insurance company where they guarantee some sort of payment.

Essentially, a equity indexed annuity (sometimes referred to as EIA’s) is sorta of a hybrid between a standard fixed annuity and a variable annuity. I say “sorta” because while do have similar characteristics, there are significant differences. According to FINRA’s website, they describe them as the following:

“EIAs are complex financial instruments that have characteristics of both fixed and variable annuities. Their return varies more than a fixed annuity, but not as much as a variable annuity. So EIAs give you more risk (but more potential return) than a fixed annuity but less risk (and less potential return) than a variable annuity. EIAs offer a minimum guaranteed interest rate combined with an interest rate linked to a market index. Because of the guaranteed interest rate, EIAs have less market risk than variable annuities. EIAs also have the potential to earn returns better than traditional fixed annuities when the stock market is rising.”

There’s no doubt that equity index annuities are confusing. When variable annuities started offering their income benefit riders (these are special add-ons that annuity products offer to give investors a guaranteed income stream), I became overwhelmed with all the mechanics behind them because every insurance company had something slightly different. To compound the problem, they were constantly making small tweaks to their offerings making it difficult to sort out which one was which.

Now imagine if it’s difficult for the advisor to understand how these products work, how do you think the clients feel? Exactly.

To best understand how these annuities work, I thought it would be best to break it down into two parts. The first part we’ll look at is the index option and explain how that works. The second part we’ll explore the “income rider” or “guaranteed benefit withdrawal” that most of these products offer. This income rider is one of the major selling points for most individuals so I definitely want to take a closer look at that.

How a Equity Indexed Annuity Works

A common selling point in regard to fixed indexed annuities is the guarantee of principal {meaning that you will never lose a dime of your money that you pay to it}.

A common selling point in regard to fixed indexed annuities is the guarantee of principal {meaning that you will never lose a dime of your money that you pay to it}.

While yes that is certainly the case, one thing that you need to be aware of is that all annuities come with some form of surrender charge meaning that if you were to cash out your annuities early, you would pay a significant surrender just to get your principal back. (We’ll look at a sample surrender schedule so that you can see exactly how much you would pay in penalties.)

Going back to the original point, yes your principal is guaranteed so as long as you keep the annuity for the entire length of the contract. As you can imagine, for many investors that scorn the stock market this is a valuable characteristic to have.

How does the index option work?

For the sake of this post, I want to keep it very simple and just explore one of the indexed options that are currently available. Please keep in mind that all indexed annuities have various indexed options and various cap strategies so understanding what you’re actually getting into is essential.

In this scenario that I have a screen shot of it shows investing $250,000 into an equity indexed annuity. This particular annuity has a ten-year contract period and is currently using a basic indexed option known as the S & P 500 point-to-point index strategy. The S&P 500 index strategy is probably the most common index that you will see used in any of the equity indexed annuity products.

I’m starting to see more now use international indexes, other market indexes such as the value index and I’ve even seen some now use a gold index.

Sample. For illustrative purposes only

In this illustration since we are taking on a ten-year contract, the investor is entitled to a bit of a higher cap on the interest rate.

For example, in this case the election of interest credit is 3.5% (usually referred to as the “cap rate”). With the rates being at all-time lows, these cap credits are significantly lower than they were in years past. With this same product, had the investor taken out a five-year product they would’ve been capped at 3% instead of 3.5%. Most insurance companies will give you a higher rate if you lock up your money longer.

So how does the interest rate cap work? Looking at the illustration in year one if an individual was to put $250,000 in and the S&P 500 index performed 7.43%, the investor would get a cap of 3.5% credited to your account. The remaining difference goes back to the insurance company. If there is a “catch” in these type of policies, that would be the big one.

In year 2, the illustration shows the the S&P 500 going up 5.35%. Once again you’re capped at 3.5% with the remaining difference going back to the insurance company.

At this point you’re probably wondering why in the heck you would want to be capped on your upside? Looking at year 9 should put that into perspective for you.

In year 9, when the S&P 500 is down 9.25%, in that year you don’t make the 3.5%, but most importantly you don’t lose anything showing a net return of zero. That’s one of the attractive features of the equity index annuities.

With equity index annuities, your principal is protected in years the market loses money no matter how steep the losses.

Quick note, personally I’m not a big fan of these types of illustrations. Why? Primarily because in the first couple of years they usually show constant growth and as we all know, the market does not work in that way. We have ups and downs. Personally, I would like to see an illustration that shows losses in the beginning to not give the potential investor high hopes in their expected returns.

Surrender Charges Beware!

In the Dateline special that I watched several years ago, one of the main things that they focused on was the disclosure of surrender charges when it came to equity indexed annuities. A lot of the bad advisors were very misleading or deceptive when sharing if there was, in fact, a surrender charge. In one case, one independent insurance agent flat out lied to the potential client telling them that they could withdraw their money at any time. This is far from it.

The first thing that you have to realize that equity indexed annuities come in different contract lengths. They can be anywhere from four years on up to 15 years. I’ve seen them all.

In the illustration above, this was a ten-year contract. I’ve enclosed a snapshot of the surrender schedule that you would be included in the documentation for the illustration above. As you can see, in the first year if you were to liquidate the annuity, there would be a 10% penalty on your interest and principal. This is very important to note.

Sample Surrender Schedule

Often times, bad advisors will sell these to seniors comparing them to CDs in their security and stability. While the one big fundamental difference is that with the CD, if you cash it out early, you just give up your interest. A fixed indexed annuity, if you surrender it early, not only do you give up your interest, but you also give up a portion of your principal, and that is a huge difference.

Now keep in mind, most of these annuities do allow for a free withdrawal, meaning that you can withdraw anywhere between 10% to 15% of your principal each year without a surrender charge, but anything over and above that will be subject to the surrender schedule.

Where Equity Index Annuities Really Flourish – Income Riders

Thus far we looked at the cap rates and principal protection that EIA’s offer. For some people (especially retirees) that’s enticing, but it might not be enough for them to invest into one. Where many retirees find comfort in EIA’s is there income riders.

How the income riders work. Sticking with our $250,000 example above, I’ll demonstrate how the income rider works.

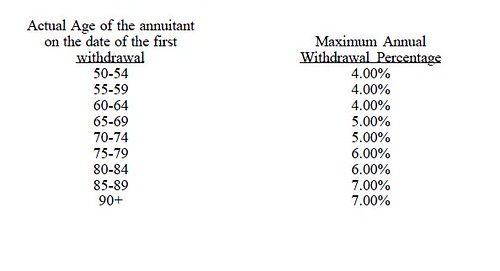

Say that a 60 year old invests $250,000 into an EIA and wants to start taking a guaranteed monthly benefit, then using the table below, they would have a $10,000 ($250,000 x 4%) guaranteed annual income for life. Even if they end up pulling out more than their principal, they would still continue to receive payments.

A 65 year-old individual with the same amount would get a bit more collecting $12,500 guaranteed per year.

Guarantees for retirement

Where income riders get even sweeter. If you’re a 60 year-old individual that has $250,000 to invest but doesn’t plan on retiring until 65 or later, then the income benefit riders becomes that much more attractive. Insurance companies will give an additional credit to the income account that, in turn, gives you a potential higher payout when you need it. Let me explain……

A 60-year old may get a 5% income credit increase each year up until the day they decide to start taking their money. That means that the insurance company will add 5% a year to original deposit (in this case $250k) each year. Once you start taking your income, the payout will be the amount in your income account multiplied by the withdrawal percentage based on your age.

The table below illustrates this over a 10 year period.

| Years Deferred | Age | Income Account Value | Annual Payment |

|---|---|---|---|

| 1 | 61 | $262,500 | $10,500 |

| 2 | 62 | $275,625 | $11,025 |

| 3 | 63 | $289,406.25 | $11,576.25 |

| 4 | 64 | $303,876.56 | $12,155.06 |

| 5 | 65 | $319,070.38 (5% payout begins) | $15,955.51 |

| 6 | 66 | $335,023.89 | $16,751.19 |

| 7 | 67 | $351,775.08 | $17,588.75 |

| 8 | 68 | $369,363.83 | $18,468.19 |

| 9 | 69 | $387,832.02 | $19,391.60 |

| 10 | 70 | $407,223.62 | $20,361.18 |

The 5% income credit is for hypothetical purposes. Each insurance company will have their own set interest rate. Recently, I’ve seen anywhere from 5% all the way up to 7%.

Another thing to consider is that the maximum withdrawal percentage is typically lower if you’re looking for a lifetime guarantee for you and your spouse. Typically, it will be about .50% lower.

Beware: The income credit and the maximum withdrawal percentage are used to determine your payout guaranteed payout. It is NOT the same thing as “making 5% on a CD”. I’ve encountered many advisors that sell these as investments with a “5% guaranteed return”.

Yes, there is a guarantee but most people associate that return like a CD or a bond would pay. These are two totally different animals. If an advisor presents this to you as a “CD like investment” I would be cautious. Very cautious.

Who Should Buy a Fixed or Equity Index Annuity?

So with all that thorough analysis, you’re probably wondering for whom does it make sense to purchase an equity indexed annuity. Typically I think if you meet some of the following criteria, then you might be a good candidate.

- You absolutely hate the stock market. If you’re tired of seeing your investments rise and fall with the Dow Jones, then an equity indexed annuity might be a good fit.

- If you have five to ten years before you actually need to draw income. Personally I think the income riders are a viable option for those that want to avoid the market and want to have a guaranteed income stream at retirement. With the income account increasing each year for each year that you’re not touching it, this can be a huge benefit for someone who has a big chunk of money that can invest it and sit on it for a few years.

- You want to diversify. You might be a strong believer in the markets, but a little certainty never hurt anyone. Taking some money and locking it up in annuity with a guaranteed income rider could make sense.

As always, make sure that you ask plenty of questions and make sure you have a solid understanding before many any investment. Annuities are long-term investments so don’t use this if you’re looking for a short-term solution.

Have you purchased an equity indexed annuity? What was your experience?

Leave a Reply